Open any news or finance app, and you’ll see it: headlines shouting about the latest share price crash or surge — it’s simply how markets work.

Ups and downs are normal. What matters is whether your savings and investments are set up to ride through them without you feeling panicked or the need to sell at the worst moment.

Finance people often talk about two golden rules in any strategy: 1. Diversification, and 2. Long-term thinking.

Diversification: don’t bet your future on one thing

Diversification is how finance people describe a simple idea: not putting all your eggs in one basket.

The Financial Conduct Authority’s (FCA) InvestSmart campaign describes diversification as: “spreading your investments across different financial products to reduce risk”.

In practice, this means avoiding a situation where your future depends on one company, one sector, or one ‘hot’ investment theme.

Long term: no need to check every day

Investing is meant to be over the long term; what matters is the value at the end compared with the value at the start, not the day‑to‑day fluctuations in between.

So when you are investing over the long-term there is less of a need to look at valuations all the time. Of course, if you want to be a hotshot investor watching and playing with the markets all the time – you may have to! There may be possible rewards to this but also be prepared to lose big money in a day too, so it may not be the way to manage your life savings. And that’s where we can help.

Experience matters

Which brings us on to managing money.

Most of us aren’t taught how to manage our money — not when it comes to long-term financial planning anyway.

So, when big decisions arrive, such as buying a first home, investing a pension lump sum, or making savings work harder, many of us are expected to just ‘figure it out’. Too many people are making important choices without the confidence or tools they deserve.

We see this all the time across the UK Police Family. When you’re juggling shift work and family life, it’s understandable that investing can feel complicated, overwhelming, and easy to put off until later.

How we structure our products to help

At Police Friendly and Metfriendly, we are dedicated to providing financial products tailored to the needs of members of the UK Police family at every stage of their careers.

We recognise the pressures of working in the Police; the limited time available to build financial knowledge; when you are likely to have the most and the least disposable income; and the financial goals you are likely to have at each stage.

With this in mind, we take the principles of diversification and long-term investing and create products that incorporate these for you without you having to plan and manage them all yourself.

Here’s how.

Diversification

All our products invest in our investment fund. The fund works away in the background to deliver returns to our members.

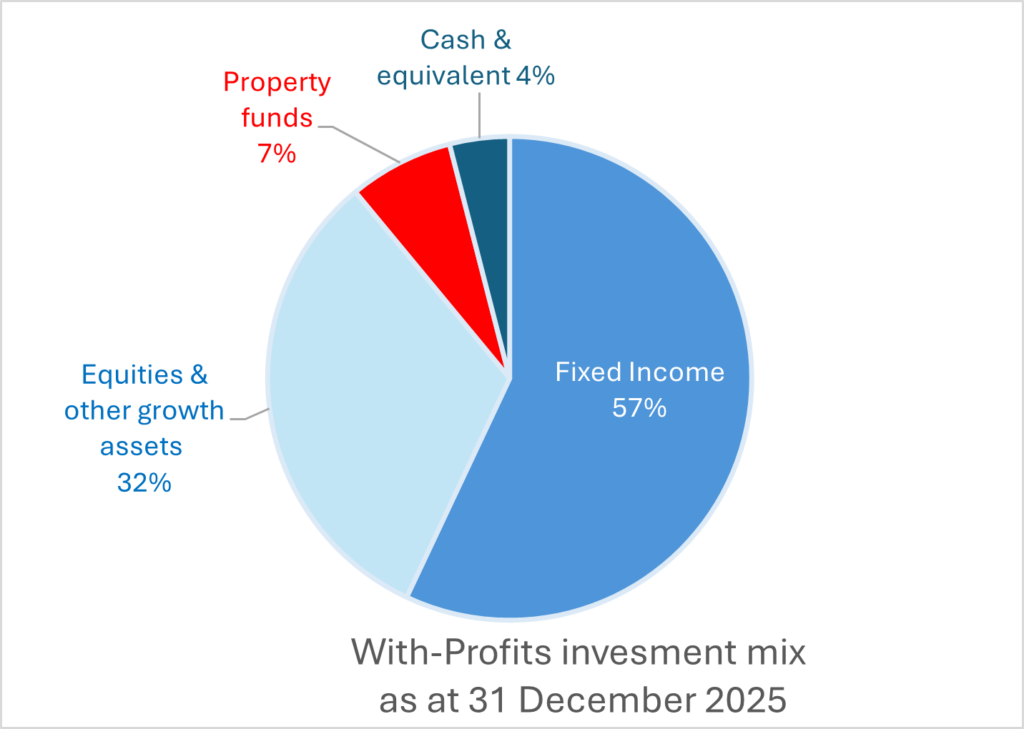

The good news: our fund is diversified- it invests money across a mix of assets, including shares, property, bonds and cash, which means we have done all the diversification legwork for you.

You can see below, in our current Investment mix, only 32% is invested in equities. This helps limit the impact of market highs and lows. Most of our members’ money is in stable fixed-income funds where the returns can be predicted with reasonable certainty.

Long-term thinking

All our products are designed to deliver a return over five years or more.

This means they are built for lifetime events – for example, buying a house, helping children through university, or retirement – rather than day-to-day expenditure that you might want to dip in and out of short-term savings for.

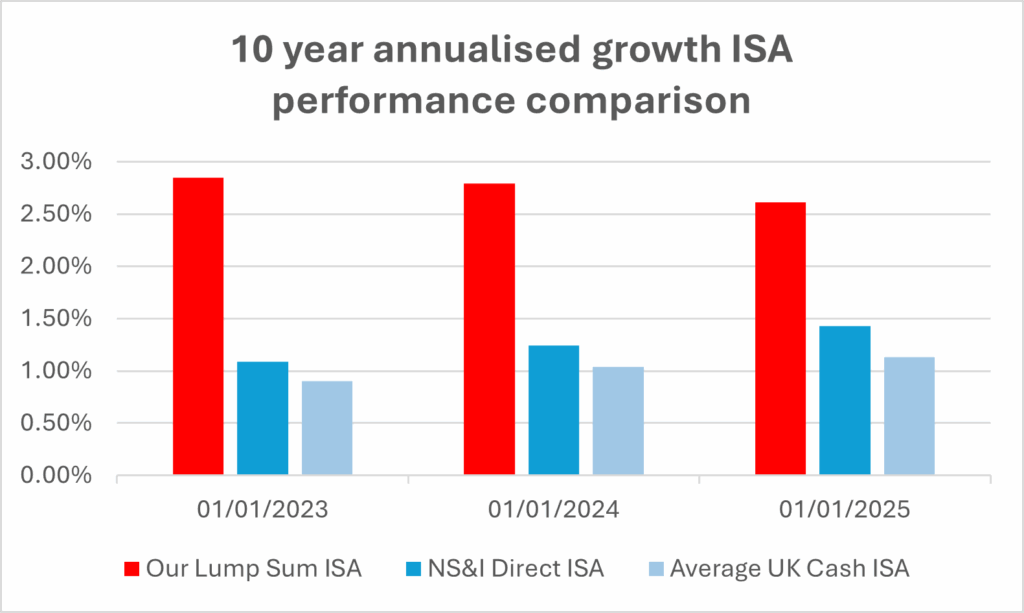

If you have lifetime events in mind, we have proved that our long-term approach works.

While past performance isn’t a promise of future returns, our comparisons show our fund has outperformed an average Cash ISA by nearly 2% over the past three years on a 10‑year annualised basis.

Our fund works slightly differently to an average Cash ISA, it doesn’t pay any interest, instead, you will typically receive an annual bonus and a potential final bonus when you’ve been invested for longer. For example, the published final bonus for a 15‑year ISA bond (single premium) is 41%.

We work with professional fund managers

To help you get what you want from your investment, we outsource the day‑to‑day management of our investment fund to professional fund managers. They focus on the detail, the discipline and the decisions — while you focus on your life and your goals.

Our chosen fund managers are Schroders, one of the world’s most established investment firms with more than £800bn in assets under management (as of 31 December 2025) and operations in 38 locations worldwide.

Schroders manages our significant investment portfolio with a clear focus on the long‑term objectives we have set on behalf of our members.

We watch the value, so you don’t have to

With our products, we provide an annual statement showing the value of your plan, including any annual bonus, so there’s no need to check on valuations daily.

The takeaway

Markets will always move — so the goal is to build a plan that spreads risk, ignores noise, and gives your money the time it needs to work.

The UK Government is now encouraging savers to consider Stocks & Shares ISAs over Cash ISAs for long‑term growth, noting that Stocks & Shares ISAs can offer “much higher” returns than cash over the long term. That long‑term difference is illustrated in the graph above.

So, while yes, investing might seem confusing and overwhelming at first, it is worth taking a proper look, because there are options available that make it far easier and less risky than you might think.

Where to start investing with Police Friendly & Metfriendly

If you want a calmer way to build wealth over time, our member-focused products are designed for different ways of saving.

They all invest in our fund that’s diversified, and, if you invest before the end of the tax year – 5th April 2026, there are some great offers too.

- Under 40 and saving for your first home, or later in life?

- Save in a Lifetime ISA and benefit from a 25% tax free Government savings bonus. The savings limit is £4,000 each tax year, so that means up to £1,000 in tax-free cash from the Government every year. What’s more, this still leaves you up to £16,000 each tax year to save in another type of ISA.

- Want to save regularly from £30 a month or invest a lump sum of £2,000 or more.

- Save tax-free in our stocks and shares ISA. You and your family members each have an ISA allowance of £20,000 each tax year, so put away as much as you can and shelter your hard-earned savings growth from the tax man.

- Lump sums beyond ISAs

- For larger one-off amounts (like a pension lump sum) when you have used all your annual ISA allowance, our With-Profit Bond is designed for investments from £2,000 and has no fixed term or upper savings limit.

This blog is for general information, not personal financial advice.